The 4FT model signals a critical phase of the cycle: rising volatility, defensive rotation, and risks for global equities

Full Slowdown: Markets Are Changing Skin

The 4FT model signals a critical phase of the cycle: rising volatility, defensive rotation, and increasing risks for global equities

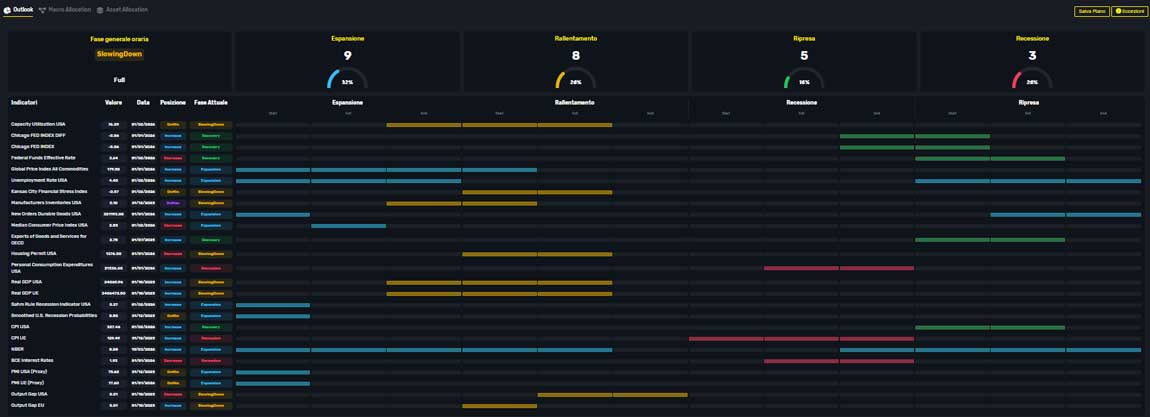

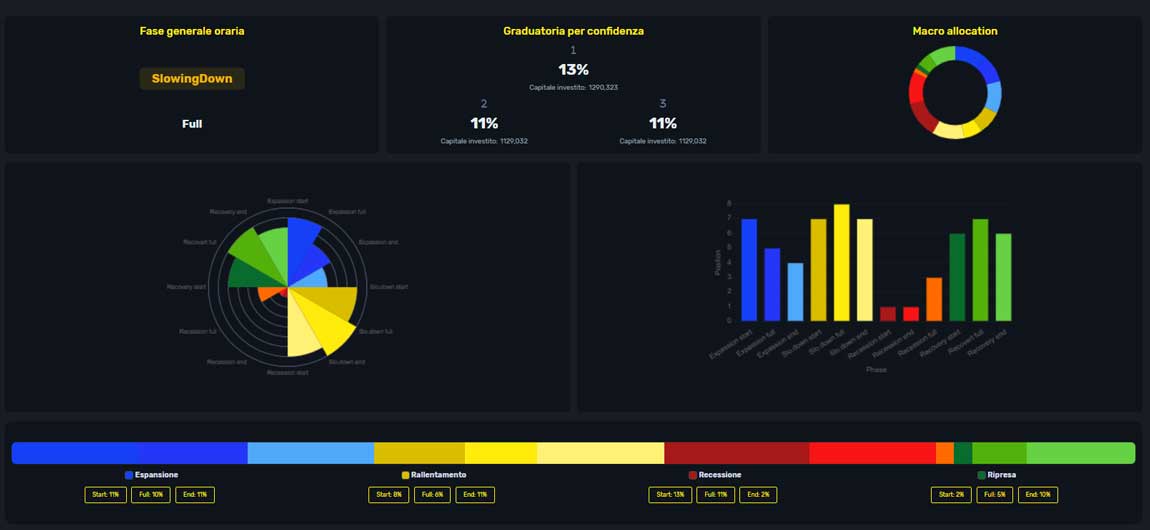

In recent months, the global macroeconomic environment has shown increasingly clear signs of deterioration. The proprietary model of 4FT Invest Ltd., based on more than 25 macroeconomic indicators from the Federal Reserve, firmly identifies the current phase as a full slowdown — a crucial turning point in the economic cycle that has historically preceded recessions.

An Increasingly Evident Slowdown

Macroeconomic data paint a consistent picture: slowing growth, weakening demand, and a progressive tightening of financial conditions. Key indicators such as industrial production, consumer confidence, labor markets, and credit conditions are converging toward a single signal: the economy is structurally losing momentum.

Adding to this is a decisive factor: still-restrictive monetary policies. Central banks, committed to containing inflation, are keeping interest rates higher for longer than expected, increasing pressure on investment, credit, and corporate profits.

Central Banks: Forced Pause, Restrictive Bias

Major central banks now find themselves in an extremely delicate position: slowing growth but still resilient inflation.

Federal Reserve (FED)

The Fed prioritizes inflation control, even at the expense of growth.

European Central Bank (ECB)

Europe faces a challenging mix of weak growth and energy shocks.

Bank of England (BoE)

Energy-driven inflation and weak GDP create a structural dilemma.

Bank of Japan (BoJ)

Japan remains an outlier, though inflation pressures are rising.

Reserve Bank of Australia (RBA)

The RBA stands out as one of the few central banks still actively tightening.

The Global Picture: A Synchronized Turning Point

Despite regional differences, a common theme emerges: the end of the accommodative monetary policy cycle

Central banks are:

This environment reinforces the 4FT model’s signal: a full slowdown is underway.

Global Equities Under Pressure

Major global equity indices reflect this transition:

Markets are no longer driven by synchronized expansion, but by defensive sector rotation and increasing dispersion.

The Return of “Fly to Quality”

In this environment, investor behavior is shifting rapidly. A classic “fly to quality” dynamic is emerging:

Industrial commodities, in particular, are signaling weakness consistent with declining global demand.

Geopolitics: The Risk Multiplier

Recent geopolitical tensions are further amplifying uncertainty. Trade fragmentation, regional instability, and energy risks are contributing to:

The combination of macro and geopolitical factors is accelerating the transition toward a more defensive phase of the cycle.

Toward the Next Phase of the Cycle

Historically, a full slowdown represents a transition phase:

weakness spreads from macro data to financial markets, laying the groundwork for a potential recession.

In this phase, risk management becomes central. Asset allocation shifts toward:

Defensive positioning is not just caution—it is a rational response to an environment where growth is no longer the dominant driver.

The information contained in this article is provided for informational purposes only and does not constitute financial advice, investment solicitation, or personalized recommendations. The analysis is based on proprietary models and data believed to be reliable, but no guarantee is given as to its accuracy or completeness. Investments involve risks, including the loss of capital. 4FT Invest Ltd. accepts no liability for any decisions made based on the information provided herein.

© 4FT Invest LTD. All rights reserved