Weak growth and energy-driven inflation reduce the room for manoeuvre for the Fed, ECB, BoE and BoJ.

PMIs Slow, Bonds Under Pressure

Weak growth and energy-driven inflation reduce the room for manoeuvre for the Fed, ECB, BoE and BoJ.

The macroeconomic week delivered markets a less linear message than equity indices alone might suggest: activity is slowing, especially in European and British services, but price pressures remain alive. This is the least comfortable combination for central banks, because it weakens the case for rate cuts without yet showing a cyclical deterioration severe enough to justify an accommodative shift.

In the United States, the picture remains the most resilient, but also the riskiest on the inflation front. The S&P Global Composite PMI remained at 51.7 in May, with manufacturing rising to 55.3, a four-year high, while services slipped to 50.9. The data point to still-positive growth, but increasingly unbalanced: part of the industrial strength comes from precautionary inventories and front-loaded purchases, not necessarily from structurally stronger final demand.

The US labour market confirms a dynamic of “resilience without acceleration”: initial jobless claims fell to 209,000 in the week ending May 16, while continuing claims edged up to 1.782 million. April payrolls had already shown 115,000 new jobs and an unemployment rate unchanged at 4.3%, signalling a labour market that is not in crisis, but less elastic than in the previous expansionary phase.

The real destabilising element, however, comes from the consumer: the final University of Michigan index fell to 44.8 in May from 49.8 in April, with one-year inflation expectations at 4.8% and long-term expectations at 3.9%. For the Fed, this is the most sensitive figure: as long as expectations become unanchored, even slower growth is not enough to decisively reopen the case for rate cuts.

In Europe, the signal is weaker. The euro area Composite PMI fell to 47.5 from 48.8, with services at 46.4 and manufacturing still above 50 but slowing to 51.4. The figure depicts a contraction in private-sector activity, especially in services, just as energy and logistics costs continue to limit disinflation.

Germany offers a picture that is reassuring only on the surface. First-quarter GDP grew by 0.3% quarter-on-quarter, supported mainly by exports, while household consumption remained flat and investment declined. The Ifo index also rose to 84.9 in May from 84.5, but remains at depressed levels consistent with fragile stabilisation, not a robust recovery.

In the United Kingdom, the split is even clearer: the Composite PMI fell to 48.5 from 52.6, with services at 47.9 and manufacturing stable at 53.7. The message for the Bank of England is particularly uncomfortable: domestic demand is slowing, but companies continue to report cost pressures linked to fuel, raw materials and geopolitical uncertainty.

Japan remains a case apart. The Composite PMI fell to 51.1 from 52.2, with manufacturing still strong at 54.5 but services flat at 50.0. Cost pressures, however, increased sharply, keeping the door open to Bank of Japan normalisation despite political caution and the slowdown in services.

For central banks, the conclusion is clear: the reaction function is once again dominated by inflation, not growth. The Fed is likely to maintain a wait-and-see stance, but with a less dovish bias; the federal funds target range is steady at 3.50%-3.75%, and the minutes show attention to incoming data and risks on both sides of the mandate. With inflation expectations rising, the market will have to accept the possibility of rates staying higher for longer, with cuts delayed and a non-negligible risk of renewed tightening if energy and wages feed through into core prices.

The ECB is probably the most trapped in the stagflationary dilemma. Rates are on hold, with the deposit rate at 2.00%, the main refinancing rate at 2.15% and the marginal lending rate at 2.40%; but PMI data point to real-economy weakness, while new European projections indicate inflation above target and lower growth. The most likely path is a prolonged pause, accompanied by firm communication on the need to avoid broad-based fiscal stimulus.

The Bank of England, with Bank Rate at 3.75% and inflation still at 2.8%, has less room to cut than the PMI slowdown would suggest. Gilts reacted positively to the weaker data, but the BoE will have to balance technical recession risks against price persistence: the base case is a pause, with hikes possible only if energy reignites wages and expectations.

The Bank of Japan remains the only major central bank still oriented, albeit cautiously, toward normalisation. The policy rate stands at 0.75%, three board members had already called for a move to 1.00%, and markets continue to discuss the possibility of action in June. The PMI slowdown does not erase the problem: Japan imports inflation through energy and the exchange rate, and an overly cautious BoJ would risk fuelling further pressure on the yen.

For the bond market, the coming months will therefore be dominated by three forces: energy inflation, slowing growth and the fiscal premium. In the United States, the 10-year Treasury remains close to 4.6%, with the 10-year/2-year curve positive by around 49 basis points according to FRED: this is no longer a curve signalling imminent recession, but one incorporating term premium, deficits and more persistent inflation.

In Europe, the 10-year Bund, around 3.04%, may benefit from risk-off phases and weak PMIs, but the return of energy inflation and the rise in public spending, especially on defence and infrastructure, limit the potential for a rally. In the United Kingdom, the 10-year gilt, near 4.90%, remains vulnerable to every inflation surprise, even though the cyclical deterioration may temporarily compress yields. In Japan, the 10-year JGB at 2.77% reflects a market pricing in the definitive end of the era of artificially low yields.

The most likely scenario is not a generalised bond-market collapse, but high and selective volatility: Treasuries still supported by inflation premium and deficits; Bunds caught between macro weakness and energy risk; gilts sensitive to every wage and price data release; and JGBs structurally under pressure as long as the BoJ remains on a normalisation path. For bond investors, duration is therefore once again a tactical choice, not an automatic safe haven.

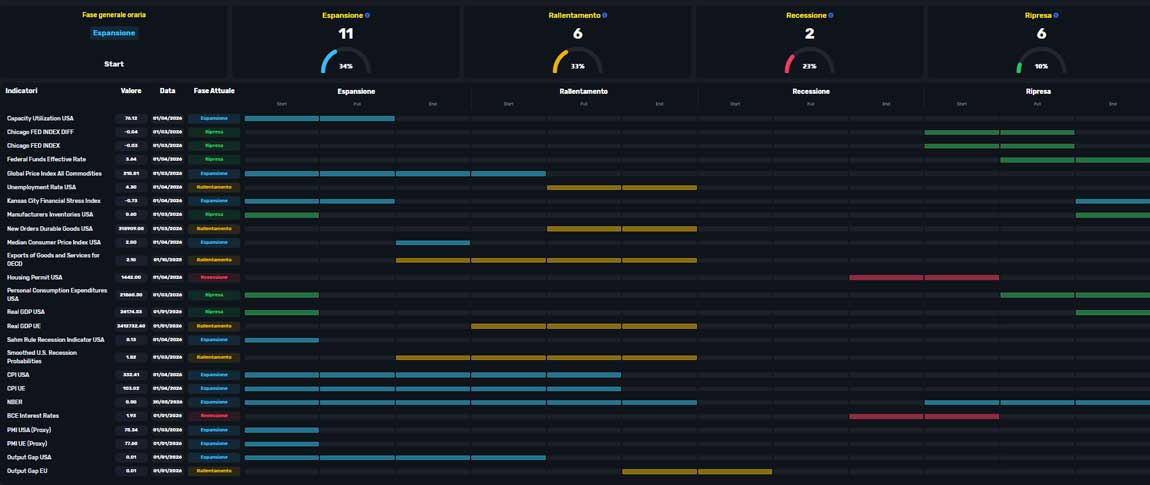

The week’s summary is that central banks no longer have the luxury of looking only at growth. PMIs point to a slowdown; the US labour market points to resilience; sentiment points to stress; expected inflation points to caution. Added to this picture is the result of the 4FT Invest Ltd macroeconomic model, based on more than 25 indicators updated directly from the Federal Reserve’s FRED database, which currently identifies an early expansion phase: a signal consistent with a cycle that is still positive, but not mature enough to reduce vulnerability to shocks in energy, rates and confidence. In such a context, the bond market will have to live with more rigid policy rates, more nervous curves and increasing sensitivity to oil, wages and expectations.

© 4FT Invest LTD. All rights reserved