Major refunds to companies after the ruling: uncertain effects on markets, currencies and commodities

U.S. Tariffs: Refunds and Dollar Impact

Major refunds to companies after the ruling: uncertain effects on markets, currencies and commodities

The return of tariffs — which never really disappeared

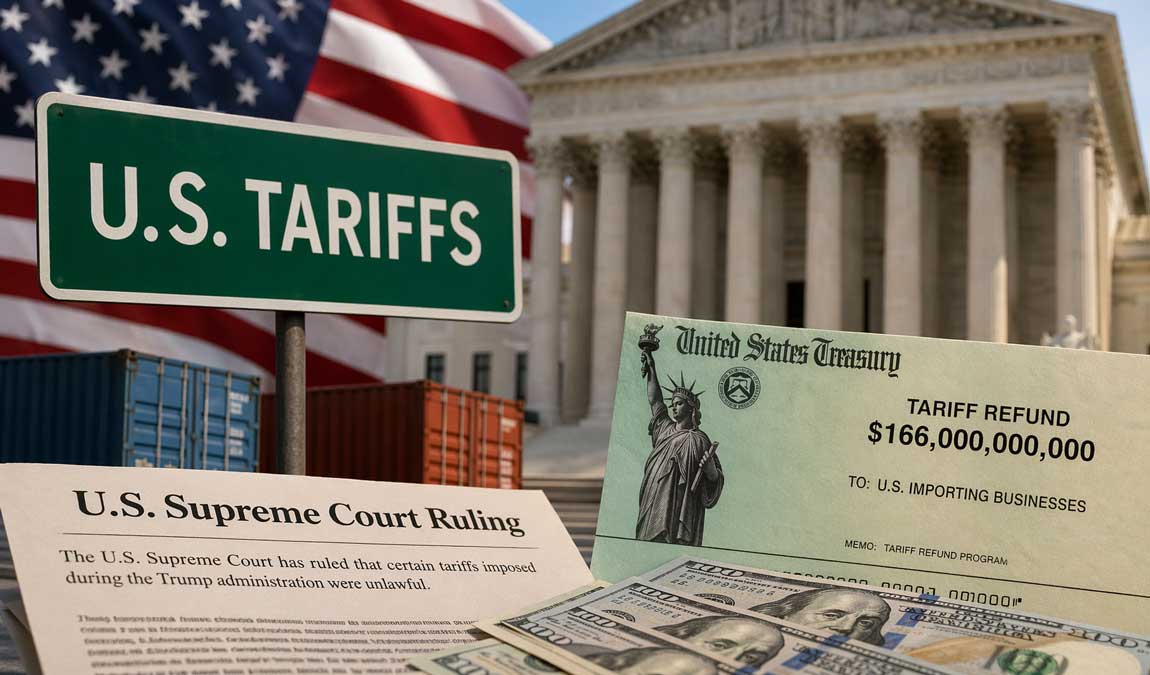

The U.S. Supreme Court’s decision to rule part of the tariffs introduced during the Donald Trump era unlawful brings back to the center of the debate an issue that markets had gradually set aside, but whose real effects have yet to fully materialize.

The key point is no longer political, but financial: a potential refund of up to $166 billion for U.S. importing companies. Given its size, this transfer could represent one of the most significant retroactive fiscal interventions in recent American history.

Yet the market is not reacting in a linear way. The reason is simple: this is not “pure” new liquidity, but a redistribution that will have differentiated and gradual impacts.

Where the $166 billion will really go

The idea of a direct stimulus to growth currently appears reductive. The evidence points to three main channels:

Recovery of corporate margins: many sectors have absorbed tariffs in recent years.

Reduction of financial leverage: in a high-rate environment, balance-sheet discipline remains a priority.

Limited disinflationary impact: the transfer to final consumers will likely be only partial.

This implies a macro effect that is more neutral than expansionary, at least in the short term.

The dollar at a crossroads: liquidity vs safe-haven status

Market operators remain focused on the U.S. dollar, whose path in the coming months will depend on the balance between opposing forces.

On one side:

greater liquidity in the system;

possible compression of real yields.

On the other:

a cautious Federal Reserve;

structural demand for dollars in risk-off environments;

the relative strength of the U.S. economy.

The result is a hybrid scenario, in which the dollar could weaken tactically without compromising its medium-term structure.

Updated FX Technical Analysis

EUR/USD

EUR/USD is trading around 1.168–1.169, after correcting from recent highs above 1.17. The first operational support lies near 1.1670, with an extension toward 1.1635–1.1665; below this range, the risk of a return toward 1.1550–1.1500 would increase. Resistance stands at 1.1760, followed by 1.1800–1.1850.

The medium-term structure remains constructive, but in the short term the pair has entered consolidation. A breakout above 1.1760 would reopen upside potential; a loss of 1.1635 would weaken the technical picture.

USD/JPY

USD/JPY is trading near 159.7–159.8, close to the year’s highs. Immediate resistance is at 159.90–160.00, a highly sensitive psychological and technical area. Above 160.00, the market would enter a zone of possible acceleration, but also of potential Japanese verbal or operational intervention. Supports are located at 159.30, 158.70 and 157.90.

The trend remains bullish, but the risk/reward profile becomes less favorable near 160.

GBP/USD

Sterling is trading around 1.348–1.350, after breaking the 1.3480 support. The short-term picture is corrective: as long as the pair remains below 1.3520–1.3540, the risk is a continuation toward 1.3420 and then 1.3350–1.3340. The next resistance stands at 1.3600.

The medium-term trend remains better than the euro’s, but in the short term bearish pressure has clearly returned.

DXY – Dollar Index

The Dollar Index is around 98.8–98.9, recovering after the rebound from April lows. The first hurdle is 99.00–99.20; above this area, the dollar could extend toward 99.80–100.00. Supports are at 98.50, 98.00 and 97.60.

The picture remains one of a tactical recovery, not yet a structural reversal: the dollar is benefiting from defensive demand linked to geopolitical tensions, but on a monthly basis it remains weak.

AUD/USD

AUD/USD is trading around 0.712–0.713. After the rally of the past month, the pair is consolidating below the 0.7180–0.7220 range, which represents the main resistance. Supports are at 0.7115, 0.7050 and 0.7000.

The structure remains positive as long as the pair holds above 0.7000, but the Aussie remains exposed to volatility linked to China, commodities and global sentiment.

USD/CAD

USD/CAD is trading around 1.369–1.371, close to the key 1.3700 resistance. A stable close above 1.3715–1.3750 would open room toward 1.3820–1.3850. Supports are at 1.3650, 1.3600 and 1.3520.

The picture remains closely tied to oil: the Canadian dollar is supported by elevated energy prices, but the tactical strengthening of the U.S. dollar is limiting the loonie’s appreciation.

USD/CHF

USD/CHF is moving around 0.786–0.787. The main resistances are 0.7900 and 0.7950; supports are at 0.7800, then 0.7720–0.7700.

The pair remains compressed: the franc maintains a defensive component, but the dollar rebound is preventing a sharper decline.

Overall reading

The dollar is not in a phase of structural strength, but in a tactical risk-off rebound. Tensions in the Middle East and elevated oil prices are temporarily supporting the greenback, while the DXY remains below 100 and still weak on a monthly basis.

The most coherent scenario for the coming months is a volatile and selective dollar: stronger against the yen and cyclical currencies during stress phases, more vulnerable against the euro, franc and commodity currencies if geopolitical risk recedes.

Commodities and geopolitics: the real driver

The dollar’s evolution remains closely tied to the global backdrop:

oil supported by tensions in the Strait of Hormuz;

gold strengthening as a hedge against instability and monetary uncertainty;

commodities still volatile, with direct effects on inflation.

In this environment, the dollar continues to fluctuate between:

its role as a safe-haven currency;

pressure from liquidity and fiscal deficits.

Outlook: what to expect in the coming months

The market appears to have underestimated the impact of the tariff ruling, but not necessarily by mistake: the effect will be slow, fragmented and not immediately visible in macro data.

For the dollar:

short term: moderate downward pressure;

medium term: resilience thanks to structural factors;

main risk: geopolitical shocks that could rapidly strengthen the greenback.

Summary and outlook

Tariffs have not disappeared: they are simply changing form. The major refund represents a potentially historic event, but with diluted, selective and complex effects. It will not necessarily produce an immediate stimulus to the real economy: much will depend on the timing of payments, the sectors involved and corporate decisions between debt reduction, margin recovery or partial transfer of benefits to final prices.

For the dollar, the effect of the refunds will probably be secondary compared with the major macro-financial drivers. The greenback will remain guided above all by three variables: Federal Reserve monetary policy, perception of geopolitical risk and the direction of global flows toward safe or risky assets.

In a scenario of high geopolitical tensions, with energy and commodities under pressure, the dollar could maintain a defensive role, strengthening especially against the yen, emerging-market currencies and cyclical currencies. In this case, gold and oil would remain supported, while global equities could show greater volatility.

In a scenario of geopolitical normalization, however, the market could return to favoring liquidity, growth and rotation into risk assets. This would reduce demand for the dollar as a safe haven and support the euro, sterling, Swiss franc and some commodity-linked currencies.

On the macroeconomic front, the decisive variable remains the Fed. If inflation proves persistent, the dollar would still receive support from real yields. If, instead, data confirm an orderly slowdown in the U.S. economy, the market could anticipate less restrictive monetary conditions, progressively weakening the greenback.

The conclusion is that the dollar is entering a less directional and more selective phase: not necessarily weak, but more vulnerable to rapid shifts in scenario. Tariff refunds may act as a marginal liquidity factor, but the main trajectory will be determined by the intersection of geopolitics, Fed policy, inflation, commodities and global risk appetite.

This content is for informational purposes only and does not constitute financial advice. Trading and investing involve risk.

© 4FT Invest LTD. All rights reserved